How did Chidiebere fall into the loan shark trap in the first place?

“I was expecting some cash from my client and it took longer than expected. That was where the idea came to try a loan app and pay back when the client paid, ” he recalled.

He said his first three attempts to get a loan were not bad because he paid back at the expected deadline. However, he got deeper into the borrowing because the client wasn’t still forthcoming and he needed to continue funding cinematography classes. Then, just as he managed to escape one loan shark, he fell into another repeatedly, and now he can’t pull out.

“For Quick Credit, I owed them ₦158,320 in total. I borrowed initially the sum of ₦65,000 and I was supposed to pay ₦93,000 in 7 days. I didn’t meet up with the deadline because it was too short obviously and it took a month. It was 30 days late and so, the overdue charges grew to ₦65,000. I had to pay a total of ₦158,000 which included the initially ₦93,000 I was supposed to pay and the overdue charge of ₦65,000,” Chidiebere said, chronicling how he was caught in the depth of a loan shark trap.

“For Kash Credit, as at the time I did the calculation, I had ₦140,000 due. It was 20 days overdue. ₦55,000 was borrowed to pay back ₦84,000 in 7 days. The overdue charges were ₦55,000 and that’s how I ended up paying a total of ₦140,000. So, the interest rate for this was ₦26,000 if you subtract ₦55,000 from ₦84,000,” he added.

Lost in the pool of debts

Sadly, Chidiebere resorted to borrowing from one loan app to pay another, until he became trapped in the pool of debt. An initial debt of about ₦65,000 has now run into over a million, borrowing from more than 20 loan apps. He didn’t realise how fast the loan seed had germinated until he lost control of the situation. Tired, he abandoned the repayment schemes, watching as interests and overdue charges increased every day across the 20 loan apps.

“I couldn’t deal with the harassment and the effect it was having on my mental state anymore. So, I decided to sell my car, to clear up all the debts and start on a clean slate,” he said. “By the time I did all my calculations, I was surprised that everything amounted to ₦1.2 million and I sold my car for ₦1.7 million. You can imagine. Anyways, I still did to just have my peace of mind.”

A Breakdown of Chidiebere’s loan apps debts calculations showing loan apps, accumulated interest rates, money borrowed and overdue charges. Photo Credit: Chidiebere’s WhatsApp (2024)

In Nigeria, money lending has evolved from the traditional banking system to a more flexible and technology-driven one. With one click, Nigerians apply for instant loans through digital financial platforms, which are now prevalent in the country.

A 2022 report by the Guardian UK revealed that many borrowers unable to access traditional bank loans were lured into debt traps by conventional loan apps. They are debt-shamed and harassed when they fail to repay or meet the demands of their lenders.

“It is unreasonable and manipulative,” Chidiebere whined. “The interest rate they give you before you take the loan is not always what you eventually see after you take it.”

He added that he never wanted to face defamations from financial institutions but that was his lot when he failed to pay back. “I wouldn’t have tried taking the loan if I knew it would turn out like this. The three months of learning became my worst nightmare,” he said.

From repeated calls to threatening messages and defamations, the debt phase was traumatising for him. However, he is just one of many other vulnerable Nigerians who have fallen into the debt trap of predatory loan sharks in Nigeria. While some managed to find a way out, others struggled through the traumatising dead ends waiting for the worst to happen.

Economic realities pushing Nigerians into debt traps?

A report by the National Information Technology Development Agency (NITDA) revealed that Nigerians’ total debt appetite has crossed a whopping ₦7.5 trillion because they find it easier to turn to fast and digital loan apps. According to the report, the number of approved loan apps has jumped by 80 percent to cater for the high debt demands of Nigerians, showing a significant increase.

The data captures the harsh economic realities pushing vulnerable Nigerians to find a way out through loans. The high debt rate also reflects the struggles to cope with the rising cost of living and declining purchasing power.

“I got arrested because of this loan,” Abboy Emmanuel, another victim of loan sharks, shared his story. He said he was managing a Petrol Station, which was a family business in Port Harcourt. He then lost track of his expenditure after attending to family needs with the business capital without proper documentation.

“My elder brother who was also working with me would come and borrow some money from the business. I would give him because he always promises to pay me back. I didn’t see the need to document any of such instances but I knew it. To my shock, the business needed funds and I went back to retrieve the money my elder brother borrowed and he denied it. He claimed he never collected any money from me and asked for proof which I obviously didn’t have,” he noted, explaining why he decided to take a loan from a digital shark.

It was a serious case at the time. He couldn’t face the family because no one was going to believe him. His elder brother who knew about the money denied it, claiming he must have syphoned the fund. Along the line, his brother arrested him, accusing him of running down the family business. In an attempt to salvage the situation, he took a loan of ₦250,000, which he has not been able to pay back to date.

The possibility of exploiting desperate borrowers is one of the major highlights in a report by the Nigerian Inquirer, noting that increase in digital lending platforms has increased financial inclusion in the country. The report also recommended that policymakers should pay more attention to the creation of a sound credit structure that is conducive to the development of lending and borrowing in a stable economy.

“The development that will help shape Nigeria’s financial market in the future lies in the ability to meet the need for credit. It is also in recognizing the growing need for consumer protection against debt traps.” the report stated.

Interest rates, terms and conditions

Many victims have complained about very high interest rates of digital loan apps which puts them in an unending debt cycle that becomes hard to break. 28-year-old accountant, Oluwatobi Samson, revealed that most of these Mobile loan apps prey on the ignorance of borrowers, who hardly read terms and conditions before taking the loans.

Samson said he applied for a loan through some digital apps when he desperately needed money to complete his final year project in school. He didn’t care about the interest rates but just applied to meet his urgent needs. “Sokoloan gave me 5,000 and told me to pay N12,000 in less than seven days, which was over 200% of what they gave me. The money was not even enough for what I needed it for,” Samson said.

After his National Youth Service Corps (NYSC), he worked with a loan app company, where he got to understand how they operate before he got his present job. He revealed that many of the loan apps are founded and owned by international companies from China. They set up the business in Nigeria, hand it to Nigerians and go back to their country where they run the business, he said.

For 29-year-old private driver Ameachi Ibuaka, the interest of loan apps was exploitative to put borrowers in a position where they have to pay much more than the apps give and most of the time, one is trapped.

“Honestly, I advise people to take terms and conditions very seriously. I’m not sure if it was my fault for not reading it properly or if these loan apps intentionally disguise their terms and conditions to suit one’s desperation. Once you take it, it is always a different story,” Ibuaka said.

Nairametrics, a Nigerian business and finance news, reported that the stipulated interest of most loan apps approximately ranges from 2 percent to 30 percent of the borrowed money but noted that most victims have said otherwise, citing an interest rate as high as over 300 percent. It also states that some of these loan apps go as far as imposing interest rates as high as 80 percent every week plunging borrowers into more loans.

Defamation, harassment and threat messages

“I started getting threatening calls later when the time they gave me elapsed. They called people that were close to me and business partners that I had absconded with their money,” Samson claimed, noting that it was beyond just meeting the timeline of repayment for these loan sharks.

For Chidiebere, the defamation messages from loan apps cost him some business deals because colleagues and business partners couldn’t trust him with their jobs.

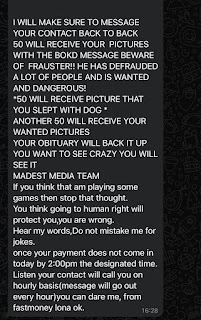

A threat message sent by FastMoney to Chidiebere. Credit: Chidiebere’s WhatsApp

“I would switch off my phone and be unavailable for weeks. I couldn’t stand the messages. Clients were bothered at some point. I couldn’t even bring myself to complete some jobs I had at hand. My debt was running into a million plus because of the high interest rates,” he said.

29-year-old Elvis Obiajulu also shared a similar experience, saying he was forced to discard his SIM cards before the defamation and threat messages stopped.

“I wouldn’t want anyone to go through that. It was the most traumatising time for me. I would be so scared to come out of my house that someone would arrest me. Everything around me triggered the thought until I eventually threw the SIM card away,” Elvis noted.

Loan apps and violation of regulatory laws

A recent article by Olusola Jegede of Resolution Law Firm explained that to operate a money lending business in Nigeria, a permit must be obtained from the Ministry of Home Affairs in a given state. It required that the business can only operate in the state where the permit is issued.

According to Jegede, these platforms must register with the Federal Competition and Consumer Protection Commission (FCCPC) and when it fails to register, it runs the risk of being banned. Jegede also believed that regulation of digital loan apps might be in place but the question would lie on its total adherence to the laws and regulations that govern its operations.

“These regulations are designed to protect borrowers, maintain market stability and promote ethical lending practices,” he said.

Meanwhile, the FCCPC in February had raised an alarm in a report about how loan apps increasingly violate its Limited Interim Regulatory/Registration Framework and Guidelines for Digital Lending 2022. According to the report, some of these violations mostly include lenders using unethical means to recover debts from borrowers and their defamation and harassment triggers. It also revealed enforcement plans to ensure that borrowers are not unlawfully exploited by these defaulting loan sharks.

However, experts believe that without strict regulations by FCCPC, these loan apps in Nigeria could further deepen the woes of vulnerable Nigerians, who are already struggling financially.

This report was produced as part of the Liberalist Centre’s Journalism for Liberty Fellowship project with funding support from Atlas Network.